Chair Walberg, Ranking Member Scott, and members of the committee, thank you for the opportunity to testify today.

My name is Heidi Shierholz, and I am an economist and the president of the Economic Policy Institute (EPI) in Washington, D.C. EPI is a nonprofit, nonpartisan think tank created in 1986 to include the needs of low- and middle-wage workers in economic policy discussions. EPI conducts research and analysis on the economic status of working America, proposes public policies that protect and improve the economic conditions of low- and middle-wage workers, and assesses policies with respect to how well they further those goals. I previously served as Chief Economist at the U.S. Department of Labor.

In considering the topic of “unleashing” America’s workforce and strengthening the economy, I make three main points in this testimony: (1) the Trump-Vance administration has inherited unquestionably the strongest economy for an incoming administration in a quarter-century;1 (2) that strength was driven in large part by economic policy choices by the prior administration and Congress; and (3) the Trump-Vance administration agenda will be profoundly destructive to the incomes and economic security for both the most vulnerable families and the broad middle class. The administration is aiming to gut key income support and safety net programs that provide direct support to tens of millions of working families, and the chaos and uncertainty they are intentionally sowing with reckless power grabs over key economic institutions will likely cause an economic crisis unless it is stopped.

The basic facts about the economy that the Trump-Vance administration inherited

The availability of jobs and the growth in real wages (i.e., growth in the purchasing power of wages after accounting for inflation) are where the rubber meets the road as far as “the economy” goes for working people. On both of these fronts, the economy that the Trump-Vance administration inherited is extremely strong.

In January 2025, when the Trump-Vance administration took office, the unemployment rate was 4.0%, and had been at or below 4.2% since November 2021. The last time the United States saw unemployment that low, for that long, was more than a half century ago. Further, the share of prime-age adults (25–54 years old) with a job was higher during January 2025 than at any time during the business cycle from 2007 to 2019, and near its highest rate in a quarter-century. The labor force participation rate of prime-age adults was also higher than at any time during the business cycle from 2007–2019, and the labor force participation of prime-age women was near its all-time high. Finally, job growth averaged 168,000 per month over the 12 months ending January 2025—a very healthy pace of growth, particularly considering how close the economy is to full employment (when job growth would be expected to slow since there is no longer a large employment gap to be filled).

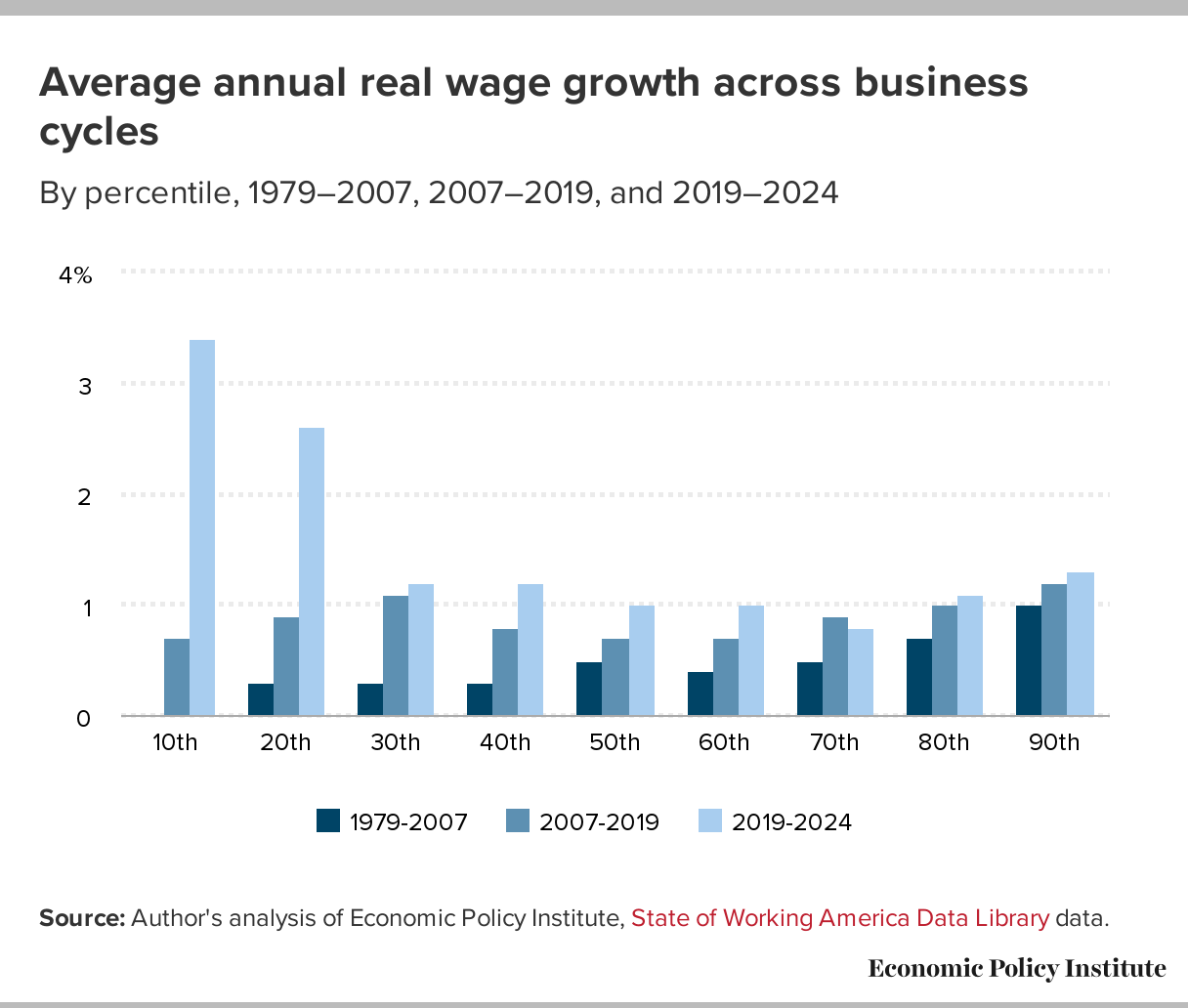

The purchasing power of workers’ wages, after taking inflation into account, was higher in 2024 than it was at the most recent business cycle peak in 2019 or any point before that. (In other words, real wages were higher in 2024 than they were in 2019 or any point before that.) Further, this was true all across the wage distribution—for low-wage workers, middle-wage workers, and high-wage workers. In fact, bucking the trend of the business cycles of the prior 40 years, wage growth since 2019 has been stronger among low-wage workers than at any other point in the wage distribution. Real wage growth for workers at the 10th percentile, for example, rose by 3.4% annually between 2019 and 2024, for a total increase of 18.2%—the fastest five-year stretch of real wage growth for this group since data started being collected in the 1970s.

Further, as Figure A shows, average annual real wage growth between 2019 and 2024 was higher across the board than it was during the business cycle from 2007 to 2019 or during the stretch of four business cycles between 1979 and 2007. In other words, real wage growth in the current business cycle has not only been more equal, it has also been stronger than in the prior four decades. And the Black-white wage gap—after increasing substantially from 1979 to 2007 and then increasing further from 2007 to 2019—meaningfully declined between 2019 and 2024.2

Average annual real wage growth across business cyclesBy percentile, 1979–2007, 2007–2019, and 2019–2024

| 1979-2007 | 2007-2019 | 2019-2024 | |

|---|---|---|---|

| 10th | 0.0% | 0.7% | 3.4% |

| 20th | 0.3% | 0.9% | 2.6% |

| 30th | 0.3% | 1.1% | 1.2% |

| 40th | 0.3% | 0.8% | 1.2% |

| 50th | 0.5% | 0.7% | 1.0% |

| 60th | 0.4% | 0.7% | 1.0% |

| 70th | 0.5% | 0.9% | 0.8% |

| 80th | 0.7% | 1.0% | 1.1% |

| 90th | 1.0% | 1.2% | 1.3% |

1979-2007 2007-2019 2019-2024 10th 20th 30th 40th 50th 60th 70th 80th 90th 0 1 2 3 4%

Source: Author's analysis of Economic Policy Institute, State of Working America Data Library data.

{kind=link}

These facts highlight the remarkable strength of the labor market at the time the Trump-Vance administration took office, underscoring that their administration was preceded by a period of historically robust employment and wage growth and historically rapid movement in extending economic progress to a broader base of America’s workers. This is exactly what an unleashing of America’s workforce looks like.

It is also worth noting that the economy didn’t just bounce back faster than it did after previous recessions,3 it also continually outperformed forecasts. For example, real gross domestic product (GDP) is currently well above where the Congressional Budget Office projected in January 2020 that it would be right now. In other words, the economy is stronger today than forecasters who didn’t know a global pandemic was about to happen expected it would be.4 Further, the share of the population without health insurance was at an all-time low as the Trump-Vance administration took office,5 owing in no small part to rapid growth in enrollment in the Affordable Care Act exchanges.6 And though the stock market matters far less to working people than wages, the fact that the stock market gets a great deal of attention makes it worth noting that the U.S. stock markets hit all-time highs just prior to the Trump-Vance administration taking office, with the Nasdaq index rising by a whopping 36% in the 12 months before the election and 30% in the 12 months before their inauguration, and the S&P 500 up by 32% and 25% over the same time periods.

What caused the strong economy and strong labor market that the Trump-Vance administration have inherited?

The COVID-19 shock sent the unemployment rate to nearly 15% in April 2020 as the labor market lost nearly 22 million jobs in two months. With the help of the CARES Act of March 2020, those jobs came flooding back after the economy reopened in May, and by August more than 10 million jobs had been regained. But the job gains slowed dramatically throughout the fall of 2020, and the economy actually lost jobs in December 2020. The gains due to reopening had run their course, but we were still nearly 10 million jobs down.

There was an additional smaller-scale stimulus package in December 2020. The real difference-maker in jump-starting the economy, however, was the large ($1.9 trillion) American Rescue Plan Act of March 2021 (ARPA). The boost to the economy ARPA provided helped drive the unemployment rate below 4% by the end of 2021. It then stayed at or below 4% for the longest period since the1960s (and was 4% as of the day the Trump-Vance administration took office). This was an unprecedented economic policy success.

Some argue that this aggressive approach to restoring full employment was what caused the inflationary surge in 2021–2022. But the evidence shows otherwise. The post-COVID inflation spike was global, affecting literally every advanced economy, and the size of the spike across countries was unrelated to how aggressively they had moved to reduce unemployment.7 In comparative terms, the U.S. inflation spike was of average size, and it was briefer than in other countries.8 In fact, as American voters were casting their ballots in November 2024, the U.S. economy was the envy of the world in terms of growth, unemployment, and the inflation rate.9

ARPA’s success in restoring full employment was the key buffer for workers against the effects of inflation, not the cause of it. It is difficult to imagine the pain that would have occurred if the U.S. had had to endure the global spike in inflation with millions more out of work, which is what would have happened without the bold steps taken by the administration and congress to generate our record-fast jobs recovery.

Further, as discussed earlier, real wage growth—growth in the purchasing power of workers’ wages—was strong and positive between 2019 and 2024. That was due to the fact that though inflation spiked, nominal (i.e., not-inflation-adjusted) wages grew even faster than inflation over this period. This strong wage growth was due in large part to the tight labor markets that were driven by ARPA. When workers have outside options, as happens when unemployment is low and job openings are plentiful, employers must provide better pay in order to get and keep the workers they need.

After the initial rescue and recovery efforts, the Biden administration pursued its troika of “industrial policy” bills—the Bipartisan Infrastructure Law, the CHIPS and Science Act, and the Inflation Reduction Act (IRA)—which drove significant investment in public goods like transportation, ports, roads, clean energy capacity, and supply chain resiliency. Such investments will make inflation from supply chain breakdowns (the kind that Americans experienced during the pandemic) much less likely. Further, they will promote America’s future competitiveness. As the global economy inevitably moves toward decarbonization, they will help position the United States as a leader in producing the technologies that will define the next industrial age, including electric vehicles, battery storage, solar power, and other clean energy sectors that could employ many U.S. workers for years to come.

Worker protections help the economy

The investment packages post-pandemic were key engines of economic growth. Further, where not blocked by a sharply divided Congress,10 those investments were structured to include incentives to create good jobs, for example by including strong incentives in renewable energy and energy efficiency projects for companies to pay prevailing wage rates. Further, worker protection agencies pursued policies that strengthened worker protections and the broader economy, which was particularly important given congressional dysfunction.

Regulations serve a crucial role in our economy, by putting laws into action. Congress passes laws, and then federal agencies set the rules for how those laws are followed. For example, if Congress passes a law directing the Occupational Safety and Health Administration (OSHA) to ensure “safe and healthful working conditions” in America’s workplaces, OSHA responds by promulgating specific rules that employers must follow in order to establish safe and healthful workplaces for their employees. Regulations therefore play an essential role in protecting workers—ensuring safe workplaces and fair pay and protecting workers’ rights to organize and join a union so they can bargain collectively with their employers.

But regulations don’t just provide essential protections; federal regulations also provide a large net benefit to the economy, as they often correct for profound market failures (like pollution or structural imbalances in market power). Rhetoric attacking regulations generally alleges that regulations are overly burdensome for employers and cost jobs. This is a myth perpetuated by those supporting an anti-regulatory agenda—an agenda that aims to take away basic rights and protections from working people. Careful research shows that federal regulations in fact provide an overall net economic benefit and that they have a modestly positive or neutral effect on employment.

To assess whether a regulation should be undertaken, agencies consider a comprehensive set of benefits and costs over a broad time horizon. For example, regulations establishing workplace safety standards may require substantial upfront investments in safety equipment, but those investments pay off over the long term through a reduction in illnesses like lung cancer and through lives saved over decades. In addition, the need for the safety equipment creates jobs for the people producing the equipment.

Each year the Office of Management and Budget (OMB) reports to Congress on the costs and benefits of federal regulations. These reports consistently find that the benefits of federal regulations far outweigh the costs. For example, in its most recent report, OMB found that for fiscal year 2023, the estimates of benefits range from $48 billion to $79 billion, while the estimates of costs range from $15 billion to $19 billion. Thus, even if one uses the most conservative estimates (the upper bound of the range of costs and the lower bound of the range of benefits), the net benefits (benefits minus costs) are $29 billion.11 Further, research on the relationship between employment and regulations generally finds that regulations have a modestly positive or neutral effect on the net number of jobs in the economy.12

When congress refuses to act, regulations also provide the only available mechanism for policymakers to protect workers’ rights and wages. For example, the most recent iteration of the Raise the Wage Act would have increased the federal minimum wage (still a meager $7.25 per hour) to $17 per hour in six steps over five years. However, like prior iterations of the bill, it died in Congress. As a small recompense, the Department of Labor was able to grant a higher minimum wage to workers on federal contracts in early 2022 through the regulatory process. The minimum wage for workers on federal contracts is indexed to inflation annually and is currently $17.75 per hour. 13

The increased minimum wage for workers on federal contracts is crucial because it ensures the government only contracts with companies that adequately compensate their employees. The increased wages for the lowest-paid government contractors reduce poverty and income inequality, while also generating higher morale, higher productivity, lower turnover, and lower absenteeism among affected workers, resulting in better government services. It also strengthens the economy overall, because it gets money in the hand of workers who are likely to have no choice but to spend it, which boosts economic activity.

The Department of Labor (DOL) undertook other key regulations in recent years. For example, it increased the threshold below which even salaried workers are eligible for overtime pay if they work more than 40 hours a week. That level, $35,568 for a full-year worker, had not been properly updated for several decades and was so low that it did not provide protections against exploitative overwork for low-paid salaried workers with some supervisory duties. In January of this year, the threshold would have been increased to $58,656, which was well within historical standards. However, it did not go into effect because it is being held up in the courts.

DOL also published a rule to help workers and employers better understand when a worker can be considered an independent contractor instead of an employee. The rule helps combat employer misclassification of workers as independent contractors, a key cause of wage theft, which often occurs when, for example, employers do not pay the minimum wages or overtime their workers would be legally entitled to as employees. An EPI analysis finds that in 11 commonly misclassified occupations, workers misclassified as independent contractors lose out on thousands of dollars in earnings and benefits per year, compared with workers doing the same job with employee status.14 Reducing these kinds of violations also reduces the ability of employers who engage in misclassification to undercut their law-abiding competitors, and strengthens the economy overall. This rule is in effect but is currently being challenged in the courts.

The Department of Labor also released a proposed rule that would require employers to develop an injury and illness prevention plan to control heat hazards in workplaces affected by excessive heat. Employers would need to, for example, evaluate heat risks and, where appropriate, implement requirements for drinking water, rest breaks, and indoor heat control, and provide training and have response procedures to help workers experiencing symptoms of a heat emergency.

The Trump-Vance agenda will hurt working families and the economy

Despite using pro-worker rhetoric, the first Trump administration consistently rolled back worker protections, proposed budgets that slash funding for agencies that safeguard workers’ rights, wages, and safety, and steadily attacked workers’ ability to organize and collectively bargain.15 It is clear that the Trump-Vance administration is using an amped-up version of that same playbook. For example, the Trump-Pence administration issued an executive order requiring federal agencies to identify at least two existing regulations to “repeal” when proposing a new regulation. The Trump-Vance administration has ratcheted that up to ten.16 We can expect that the Trump-Vance administration, while also employing strong pro-worker language, will build upon the Trump-Pence administration’s attacks on workers’ safety, wages, and rights.

While we don’t know exactly what the new administration has planned, we can nevertheless be quite certain in some cases, based on the track record of the first Trump administration. For example, it is highly unlikely that the Trump-Vance administration will defend the overtime regulation that is currently being held up in the courts, because there was a similar overtime regulation in a very similar situation when the first Trump administration took office, which they did not defend. In other words, we can expect to see the Trump-Vance administration let this regulation, which would have provided overtime protections to millions of workers, die.

The Trump-Vance administration has already officially delayed the defense of the independent contractor rule,17 and is likely to drop that defense entirely, given that the first Trump administration promulgated a rule that provided much weaker protections to workers in 2021. They might restore the weaker 2021independent contractor rule, or might choose to let courts analyze questions relation to independent contractor classification without agency guidance. Either way, they would be abandoning a rule that helps combat misclassification of workers as independent contractors, costing affected workers thousands of dollars annually.

The Trump-Pence administration did not address regulations related to workplace heat hazards, but their track record on other workplace safety and health issues was abysmal. For example, after having halted all work in 2017 on a permanent infectious disease standard that would have protected workers from COVID-19 and mitigated the spread of the disease at work and back out into the community, and despite the widespread reach of COVID-19 in the workplace, the Trump administration’s OSHA refused to issue any required measure to protect workers from the virus. It also proposed a rule allowing teenage workers to perform unsafe tasks in health care occupations, decreased worker safety inspections, weakened standards for mine safety inspections, repealed a requirement that employers report workplace injuries and illnesses, and more.18 Given Trump’s record on worker health and safety, it is highly unlikely the Trump-Vance administration will finalize the Biden administration’s proposed rule to protect workers from extreme heat. This will result in preventable deaths due to heat exposure on the job.

The Trump-Vance budget plan will hurt America’s families and the economy

The U.S. economy has generated highly unequal growth for decades and our system of social insurance and income support is uniquely stingy among the rich countries of the world. While our international peers have chosen to increase the share of national income devoted to public goods and social protections—and to finance it with taxes—federal revenues as a share of GDP in the U.S. are where they were 70 years ago.19

Today, the U.S. “fiscal gap”—the increase in net revenue through tax increases or spending cuts that would be required to keep public debt stable as a share of gross domestic product—is large but manageable, at roughly 2.1% of GDP.20 It is important to note that the current fiscal gap was entirely created by the Bush tax cuts of 2001 and 2003 and the Trump tax cuts of 2017. The additional revenue we would have if these tax cuts hadn’t been enacted would mean the U.S. would have no fiscal gap today—i.e., we would have a fully sustainable fiscal situation—and on top of that, we would have roughly $500 billion more each year to spend on socially useful public investments.21

Putting these facts together shows that to achieve smaller deficits in a way that increases social welfare and strengthens the economy, we should be leaning on long-overdue revenue increases, particularly from highly progressive sources, like increased taxes on capital income, wealth, and higher top ordinary rates.

The Trump-Vance administration agenda, however, does exactly the opposite. They have made it abundantly clear that one of their core priorities is to cut the benefits that ordinary people depend on in order to fund tax cuts that primarily benefit the rich, while also allowing the deficit to balloon. They plan to double down on the Tax Cuts and Jobs Act of 2017 (TCJA), which delivered tax cuts that overwhelmingly favor the very wealthy (in 2025, households in the top 1% of the income distribution will receive an average tax cut of $61,090 as a result of the TCJA and the top 0.1% will receive an average tax cut of $252,300, while middle-income people will receive an average reduction of less than $1000 and low-income people will receive an average reduction of less than $100).22

The House Budget Committee, led by Republicans, voted along party lines two weeks ago to advance a sweeping budget plan that does the Trump-Vance administration’s bidding by taking the massive tax giveaways of the TCJA to corporations and the wealthy to the next level, with $4.5 trillion in tax cuts over the next 10 years.

The Trump-Vance backed House budget plan would increase the deficit by trillions over the next 10 years, which would increase the fiscal gap dramatically. Further, given today’s historically low unemployment rate, deficit-financed tax cuts are more likely to put a drag on growth going forward. The 2001, 2003, and 2017 tax cuts were all deficit-financed, but because they were enacted during times of aggregate demand slack, they did not drag on economic growth. That would not be the case this time. Large deficit-financed tax cuts would likely push aggregate demand above the economy’s capacity to produce, which would either manifest as higher inflation or—if the Federal Reserve intervenes quickly and forcefully to forestall upward pressure on inflation—higher interest rates. Higher interest rates would crowd out private-sector investment as the cost of borrowing to finance these investments would rise. Over time, the depressed investment would slow economic growth as future generations of workers have less capital to work with.23

The Trump-Vance administration-backed budget plan also seeks to cut mandatory spending by at least $1.5 trillion over 10 years to partially offset the cost of the tax cuts. This would mean massive cuts to social services. Social spending by the federal government in the U.S. is stingy relative to other advanced economies, but it is highly effectively targeted at lower-income households. Cuts to this spending would therefore cause great damage to the most vulnerable households—for example, tens of millions losing their health coverage through Medicaid, tens of millions receiving less help in buying groceries from SNAP (or being cut off completely), and many others seeing the cost of their student loans rising.

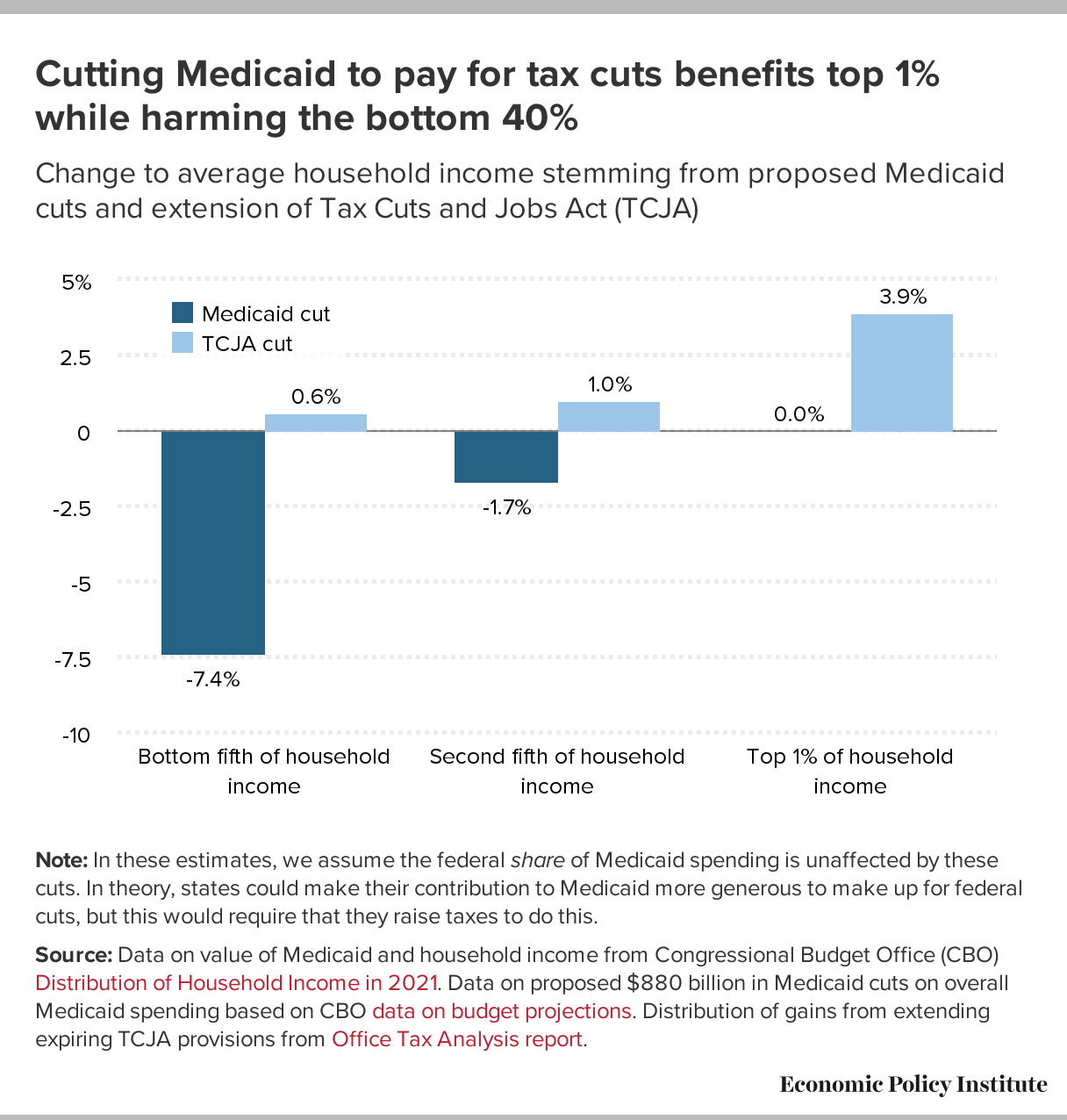

Consider the cuts to Medicaid. Health coverage is expensive in the U.S., and the value of Medicaid’s coverage is equal to a huge share of the total income of poorer families. In fact, a family health insurance plan in private markets can cost more than what the bottom 20% of families earn in an entire year.24 Figure B shows the House budget resolution’s average cut to Medicaid benefits for the bottom 40% of the income distribution, expressed as a share of average income. It also shows how much extending the TCJA’s expiring provisions would boost incomes for these groups, and the top 1%. The bottom 40% would be unequivocally worse off: Proposed cuts to Medicaid alone would reduce incomes for the bottom 40% far more than extending the TCJA would boost them.25 And of course, many of these families will also be hit with other cuts.

Cutting Medicaid to pay for tax cuts benefits top 1% while harming the bottom 40%Change to average household income stemming from proposed Medicaid cuts and extension of Tax Cuts and Jobs Act (TCJA)

| Medicaid cut | TCJA cut | |

|---|---|---|

| Bottom fifth of household income | -7.4% | 0.6% |

| Second fifth of household income | -1.7% | 1.0% |

| Top 1% of household income | 0.0% | 3.9% |

-7.4% -1.7% 0.0% 0.6% 1.0% 3.9% Medicaid cut TCJA cut -10 -7.5 -5 -2.5 0 2.5 5% Bottom fifth of household income Second fifth of household income Top 1% of household income

Note: In these estimates, we assume the federal share of Medicaid spending is unaffected by these cuts. In theory, states could make their contribution to Medicaid more generous to make up for federal cuts, but this would require that they raise taxes to do this.

Source: Data on value of Medicaid and household income from Congressional Budget Office (CBO) Distribution of Household Income in 2021. Data on proposed $880 billion in Medicaid cuts on overall Medicaid spending based on CBO data on budget projections. Distribution of gains from extending expiring TCJA provisions from Office Tax Analysis report.

{kind=link}

The damage spending cuts would cause goes even further than the current effect, because they would weaken the workforce of future generations and threaten the very strong economy inherited by the Trump-Vance administration.

Much of social spending in the United States does not just provide contemporary boosts to economic opportunity and security, it also constitutes a valuable investment in the long-run productivity of the workforce as a whole. For example, a well-developed literature finds that children’s access to SNAP leads to better health outcomes, earnings, neighborhood quality, and home ownership, and reduces incidence of poverty and incarceration in adulthood. And the longer children have access to SNAP as an income support, the better their outcomes are. All in all, it has been estimated that every $1 spent on SNAP that goes to young children yields $56 in net social benefits.26

Similar findings hold for Medicaid. Access to Medicaid as children leads to significant long-run benefits—seeing improved school performance, educational attainment, earnings, and better health later in life. Studies have found that Medicaid coverage of pregnancy and infants provides benefits that fully pay for the expenditures in the long run.27

It’s also important to note that work requirements for Medicaid—which proponents typically claim will do things like “encourage people to get back into the work force, increase labor force participation and give people again the dignity of work”—in fact have nothing to do with getting people into the workforce.28 While increasing labor force participation and helping people obtain the dignity of work are important goals, people don’t actually need encouragement to do this. The incentive to work is already there: It gives people sufficient income to not live in grinding poverty. People with income low enough to qualify for social safety net benefits also do not need new rounds of bureaucratic paper pushing, which is what work requirements mainly achieve. A careful review of the research on work requirements finds that almost none of the alleged employment benefits of ratcheting up work requirements are economically significant. If proponents of work requirements for Medicaid were actually serious about improving access to work, they would work to address the core barriers to work that low-income workers have traditionally faced: weak macroeconomic conditions, the volatile nature of low-wage work, and other barriers to work like caregiving responsibilities. 29

More broadly, a strategy that pairs large tax cuts for the rich that are substantially paid for with large cuts to programs serving low- and moderate-income families will leave the U.S. much more exposed to a recession. A dollar spent on providing a tax cut to rich families has a much lower “multiplier”—it generates less spillover economic growth—than one spent on providing income support for low- and moderate-income families. The reason is simple—rich households’ spending does not respond one-for-one to marginal changes in their income—they have large savings rates that they can adjust to absorb income changes without radically changing their spending. Low- and moderate-income families live paycheck to paycheck and do indeed fully adjust their current spending to whatever happens to their incomes, good or bad.

Hence, the spending destroyed by cutting benefits to low- and moderate-income families will be far larger than the new spending supported by granting rich households tax cuts. Initially, this downward spending shock could likely be absorbed by the Federal Reserve cutting interest rates. But paying for a large portion of the tax cuts with spending cuts would require the Fed to use the lion’s share of the space they have to cut interest rates, leaving monetary policy with limited tools to counteract any further economic weakness.

At best, this would leave the economy at the cusp of recession with all of the Fed’s conventional tools for boosting a recovery nearly exhausted. This would be an extremely unwise policy decision—one made completely for the purpose of keeping taxes on high-income households and corporations historically low.

It is worth reiterating that the administration isn’t backing these draconian cuts in the name of responding to a national emergency or reducing deficits to boost future growth. They are backing these draconian cuts to provide tax cuts that overwhelmingly favor the extremely wealth. They take food out of the mouths of poor children to line the pockets of billionaires, while simultaneously weakening our economy. It is a disgrace.

The potential financial crisis DOGE poses

Elon Musk’s recent spate of illegal impoundments and firings is an economic crisis in waiting. Spending being controlled by the whims of a billionaire who bullied his way into being able to access the Treasury accounts that get spending where it is legally obligated to go and potentially throttling this spending at its source is a disaster in the making. Spending reductions strangle economic activity and, if large and sudden enough, could push the economy into a recession and crisis. And because these spending reductions would only relent at the whim of Musk’s teams, the automatic stabilizer function of the federal government—particularly the fact that spending on unemployment insurance and other social insurance provisions rise as people lose jobs and income when the economy enters a recession—could not be relied upon to kick into gear.30

So far, the illegal impoundments have not added up to a scale that would throw the economy into a recession, but, again, this is entirely because the Musk team has so far decided to not impound that much spending. If they decide to impound more and cause a crisis, what’s to stop them? Having one person in charge of whether or not the U.S. government actually spends the money that’s been legally obligated by Congress is not just a democratic disaster, it is absolutely a recipe for an economic crisis.

To date, the real damage done by the illegal impoundments and firings is the valuable work of federal employees that is not being performed.31 Our federal workforce was too small and too poorly-paid even before the Trump administration allowed Musk’s teams to start arbitrarily hacking at it.32 Further constricting it will lead to a profoundly less functional government – and that matters a lot to peoples’ lives. But if the DOGE team isn’t stopped, their cuts won’t just sap the long-run productivity and of the economy, they could easily cause a full-blown crisis.

Conclusion

The Trump-Vance administration inherited the strongest economy for an incoming administration in 25 years—an inheritance largely driven by the economic policy choices of the previous administration and Congress. However, their agenda threatens to undermine this progress, jeopardizing the economic security of both vulnerable families and the middle class. The draconian cuts in social programs they are backing aren’t being done in the name of responding to a national emergency or reducing deficits to boost future growth, they are being done to provide tax cuts that overwhelmingly favor the extremely wealthy. They are cutting food aid to poor children and taking away healthcare from poor families to finance tax cuts that will overwhelmingly go to the very wealthy. Further, by gutting essential income support and safety net programs while sowing chaos in key economic institutions, they are setting the stage for a preventable economic crisis.

I implore you to recognize these risks for what they are and take action to protect the stability and well-being of America’s workers and families.

Notes

1. Josh Bivens, “President-elect Trump is Inheriting a Historically Strong Economy,” Working Economics Blog (Economic Policy Institute), January 17, 2025.

2. Economic Policy Institute, “Black-White Wage gap – Black-White Wage Gap, Average,” State of Working America Data Library, 2025.

3. Center on Budget and Policy Priorities, Chart Book: Tracking the Recovery From the Pandemic Recession, April 2024.

4. Jared Bernstein, “No Delusions: Bidenomics Wasn’t Perfect, But It Did Many Great Things,’ Substack, February 12, 2025.

5. Jennifer Tolbert, Sammy Cervantes, Clea Bell, and Anthony Damico, Key Facts about the Uninsured Population, KFF, December 2024.

6. Jennifer Tolbert, Sammy Cervantes, Clea Bell, and Anthony Damico, Key Facts about the Uninsured Population, KFF, December 2024.

7. Josh Bivens and Asha Banerjee, Lessons from the Inflation of 2021–202(?), Economic Policy Institute, April 2023.; Stiglitz, Joseph E. and Ira Regmi, “The Causes of and Responses to Today’s Inflation,” Industrial and Corporate Change, Volume 32, Issue 2, April 2023, Pages 336–385, https://doi.org/10.1093/icc/dtad009

8. Organisation for Economic Co-operation and Development, “Year-on-year OECD headline inflation stable at 4.7% in December 2024,” February 5, 2025; Organisation for Economic Co-operation and Development, “OECD headline inflation broadly stable at 4.5% in October 2024,” December 4, 2024.

9. Francois de Soyres, Joaquin Garcia-Cabo Herrero, Nils Goernemann, Sharon Jeon, Grace Lofstrom, and Dylan Moore, “Why is the U.S. GDP Recovering Faster than Other Advanced Economies?” Board of Governors of the Federal Reserve System, May 17, 2024; Joe Brusuelas, “American Outperformance in the Global Economy,” RSM, November 4, 2024.

10. Such as when a provision offering a bigger tax credit for EVs made with union labor was stripped out of the final IRA.

11. Dylan Desjardins, Digesting the Federal Government’s Annual Report on the Benefits and Costs of Federal Regulations, George Washington University Regulatory Studies Center, January 6, 2025.

12. Josh Bivens, “Testimony before the Judiciary Subcommittee on Regulatory Reform, Commercial and Antitrust Law,” February 24, 2016.

13. Department of Labor, Wage and Hour Division, “Final Rule: Increasing the Minimum Wage for Federal Contractors (Executive Order 14026)” (web page), accessed on February 21, 2025.

14. Adewale A. Maye, Daniel Perez, and Margaret Poydock, Misclassifying Workers as Independent Contractors Is Costly for Workers and States (fact sheet), January 22, 2025.

15. Margaret Poydock, “President Trump has Attacked Workers’ Safety, Wages, and Rights Since Day One.” Working Economics Blog (Economic Policy Institute), September 17, 2020.

16. Economic Policy Institute, “EO Unleashing Prosperity Through Deregulation,” Federal Policy Watch, February 5, 2025.

17. Economic Policy Institute, “Department of Labor Delays Defense of Independent Contractor Rule,” Federal Policy Watch, January 29, 2025.

18. Celine McNicholas, Lynn Rhinehart, and Margaret Poydock, 50 Reasons the Trump Administration is Bad for Workers, Economic Policy Institute, September 2020.

19. U.S. Office of Management and Budget and Federal Reserve Bank of St. Louis, “Federal Receipts as Percent of Gross Domestic Product [FYFRGDA188S],” retrieved from FRED, Federal Reserve Bank of St. Louis, February 21, 2025.

20. Bobby Kogan and Jessica Vela, What Would It Take to Stabilize the Debt-to-GDP Ratio?, Center for American Progress, June 2024.

21. Josh Bivens, There Will Be Pain: Continuing Low Tax Rates for The Rich And Corporations Will Hurt Working Families, Economic Policy Institute, February 2025.

22. Jean Ross, The Tax Cuts and Jobs Act Failed To Deliver Promised Benefits, Center for American Progress, April 2024.

23. It is worth noting that the crowding out of private-sector investment due to higher deficits is not always a major concern. If deficits are run to finance large increases in public-sector investment or to subsidize private-sector investments that would be otherwise under provided due to market failures—like investments in green energy generation—then the crowding out of private-sector investments does not lead to lower investment levels overall in the economy; investments just shift. If this shift leads to more capital that generates greenhouse gas abatements (like clean energy generation) and less “conventional” capital that generally supports higher greenhouse gas emissions, this shift can be very useful. But deficits run simply to finance low taxes for rich households and corporations simply crowd out private-sector investment.

24. KFF, 2024 Employer Health Benefits Survey, October 2024

25. Josh Bivens, There Will Be Pain: Continuing Low Tax Rates for The Rich And Corporations Will Hurt Working Families, Economic Policy Institute, February 2025.

26. For the list of citations and a fuller description of the research literature on how SNAP and Medicaid spending on children leads to improved outcomes as adults, see: Hilary Hoynes, “Examining the Powerful Impact of Investments in Early Childhood for Children, Families, and Our Nation’s Economy”, Testimony delivered to the U.S. House of Representatives Committee on the Budget, July 20, 2022.

27. Josh Bivens, There Will Be Pain: Continuing Low Tax Rates for The Rich And Corporations Will Hurt Working Families, Economic Policy Institute, February 2025.

28. Hilary Wething, “Work Requirements for Medicaid Do Not Address the Real Barriers to Work and Risk Throwing Many into Health Insecurity.” Working Economics Blog (Economic Policy Institute), February 3, 2025.

29. Hilary Wething, “Work Requirements for Medicaid Do Not Address the Real Barriers to Work and Risk Throwing Many into Health Insecurity.” Working Economics Blog (Economic Policy Institute), February 3, 2025.

30. Bivens, Josh. “Before DOGE, the Debt Ceiling Used To Be the Only Quick Way Political Extremists Could Cause a Financial Crisis,” Working Economics Blog (Economic Policy Institute), February 24, 2025.

31. McNicholas, Celine, and Patrick Oakford. “A Snapshot of the Federal Workforce that is Now Under Attack from the Trump Administration,” Working Economics Blog (Economic Policy Institute), February 21, 2025.

32. Josh Bivens, “DOGE is Not Worth Engaging. You Can’t Cut Your Way to a Federal Government That Does More.” Working Economics Blog (Economic Policy Institute), January 30, 2025.